In this two-week curtain, the Dow Jones (USA) dropped from 27,110 points to 25,870 DAX (Germany) from 12,850 points to 12,167 points. The loss in both stock indexes is about 5%.

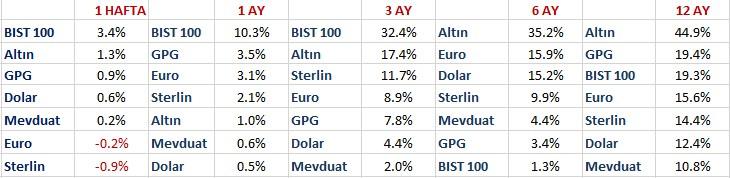

However, BIST, which completed the first week of June at the level of 110,000, gained 3.2 percent in the last two weeks and reached 113,600 points.

As such, the Turkish stock market has become one of the three most durable markets of 2020 among the 38 countries I watch. (right column below)

Let’s start with abroad. Because if the course with salesmen will continue abroad, this will affect Turkey, albeit with a delay.

I think there are three reasons why the global stock market indices passed this two-week set moderately negative.

1- The 3-week sharp rise experienced before

2- The slower than expected rate of spread of the virus

3- The agreement on the EU recovery fund has not yet taken place.

The first ingredient is the most effective if you ask me. Although the virus continues to exist in Europe, its rate of spread has slowed. Mortality rates have also come down significantly.

If we look at it as a whole, the Covid 19 epidemic continues around the world, and this causes the economy to return to normal flow in slow motion.

If you ask why the stock markets do not sell harder, the critical factor here is not how many people died or got sick. Whether the virus will cause a quarantine that will stall economies again.

Country managers around the world are of the opinion that the social cost will be higher if the economies stop again to slow the spread of the virus, and they avoid quarantines that will stop the economies again unless an extraordinary jump occurs.

However, no matter how we look at it, Covid 19 continues to have an impact on people’s behavior, regardless of restrictions. This slows the recovery rate of economies.

What balances this empty half of the glass is the abundance of money incentives and knowing that this process is temporary.

Don’t look at what the chronic pessimists say what would have happened if the markets were mischievous and central banks hadn’t done this.

I wonder what they were waiting for. There would be a fire, but would the fire brigade not come?

Financial markets are still pricing in what the second half of 2020 and the beginning of 2021 will look like in the world economy. Pricing for the full 2021 has not yet started.

This trend is likely to continue for a while. Until the last quarter of the year, I believe that the fluctuations, which we can count horizontally (within a line such as 24,000 – 28,500 in the case of Dow Jones), will continue until the last quarter of the year, although the main course in the financial markets is moderately positive.

Pricing for the whole of 2021 (growth will pick up by mid-year) means a new rally. I think the flare will be US bond yields. The compression trend, which you can see in the chart above, makes me question whether the party can start earlier, surprisingly, even though I expect the next three months to be horizontal in the world stock markets.

Unless I personally see a sharp jump in bond rates, I will continue to build my strategy according to the horizontal scenario (buying on the declines and selling on the rises) for a while.

I will read the retracements up to 0.55-0.60% in the US 10Y interest rate, which completed the last week at the level of 0.69 percent, as a reflection of the negative intermediate flow of the horizontal course and a buying opportunity in the stock market indices.

There is also an important message for those who are interested in the gold front here. I explained the relationship between the US interest rate and gold in the Compass dated May 26.

The FED will keep the interest rate close to zero until 2023, which means that the open view of gold is misleading.

Gold moves mainly in the opposite direction with the US bond yield, not with the FED rate.

If the US bond yield is pulled back to 0.60 percent in the next three months, although gold has a chance to attack again and travel to around $ 1835, I believe that we are nearing the end of the two-year rally on this front, that the yellow storm will be 1500 in 2021 and 1350 in 2022. I think it can go as low as $.

Don’t let this sentence make you think that I’m expecting $1835 in gold in the short term. I see its realization as an attractive opportunity to sell. But I wouldn’t be surprised if it doesn’t settle above $1750.

The front that will dominate the global markets in July will probably be Europe.

No agreement was reached in the teleconference of EU leaders on Friday. Each member put forward their opinion and basis.

Towards the middle or end of July, EU leaders will meet again to decide how much of the EU recovery fund is a grant and how much is a loan.

Agreement will be reached with high probability. Germany showed its stance. Europe is a union where every country can express itself, but the decisions are made by Germany.

This step is extremely important as it will open a window to the common fiscal policy in the EU. It is a candidate to create palpable market effects, especially Spain, France and Italy assets.

Similarly, if around 1.1035 is tested on the EURUSD front in the next two weeks, this may be favorable for the transition from USD to Euro.

Although financial markets see this issue off the radar for 1-2 weeks, I think that as the date approaches, we can sail into a curtain where European assets are positively differentiated with expectation pricing.

Let’s finish with BIST. Borsa İstanbul has three separate fronts within itself.

I mentioned in the previous article the large number of bubble-priced small company stocks and the damage they can cause. While BIST recorded a 3.4 percent increase in value last week, it is remarkable that 130 stocks ended the week with a depreciation.

Spread over time and timing differs on a stock basis, I predict that the attenuation of companies with bubble prices will continue, albeit without turning into a massive downpour.

Another development that marked the past three months was the positive divergence of industrial stocks and negative bank stocks.

We witnessed a jump in banks on Friday. Although many factors continue to put pressure on their profitability, I think that this lagging front may close some of the gap with industrial companies in the next 3-6 months.

For this reason, I think that some options in BIST, including some remaining industrial companies, are worth risking & carrying, but it would be misleading to repeat this for the stock market in general.

GPG CONVERSION COMPLETE

In the first half of 2020, I mentioned that I plan to transform GPG into a global investment fund that can invest in almost every country without being limited to Turkish markets. This process is complete.

GPG, which makes 10 percent of its current investments in the European stock market and 2 percent in the Turkish stock market, now represents our country abroad with the status of foreign investor.

[kanews-currencies usd=”true” euro=”true” gbp=”true” eur-usd=”true” ise-100=”true” gau=”true” btc=”true” eth=”true” bch=”true” xrp=”true” ltc=”true”]

[kanews-related-post tag=”div” ids=”211″ title=”İlişkili Yazı”]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment